Improving customer understanding to reduce cancellations.

A discount the company sells on, that customers don't understand.

The no-claims discount is one of the strongest selling points for Marshmallow's target audience, and a meaningful part of how we win against competitors — particularly for customers who are new to the UK and bringing claim-free history from another country.

But it's also one of the most misunderstood parts of the product. Customers were declaring discounts they couldn't verify, getting their prices increased mid-policy, and cancelling. Trust was being damaged. The numbers were going the wrong way.

A growing trend, and a clear root cause.

The proportion of direct customers cancelling their policy in the first month had climbed from 13% to 21% over the course of 2024. Most cancellations happened after we increased the price of someone's policy — which we'd done because we couldn't verify the no-claims discount they'd declared at sign-up.

Alongside the cancellations, complaints about no-claims discount were rising and we were seeing negative reviews from customers who didn't even know a discount had been applied to them in the first place.

When we looked at the flow, the cause was clear. The questions we asked were oversimplified. The eligibility requirements were buried behind 'learn more' links. Reminders to upload supporting documents were confusing and often went to spam. Customers were being asked to declare something they didn't understand, with no obvious way to verify it correctly.

Four things we learned from talking to customers.

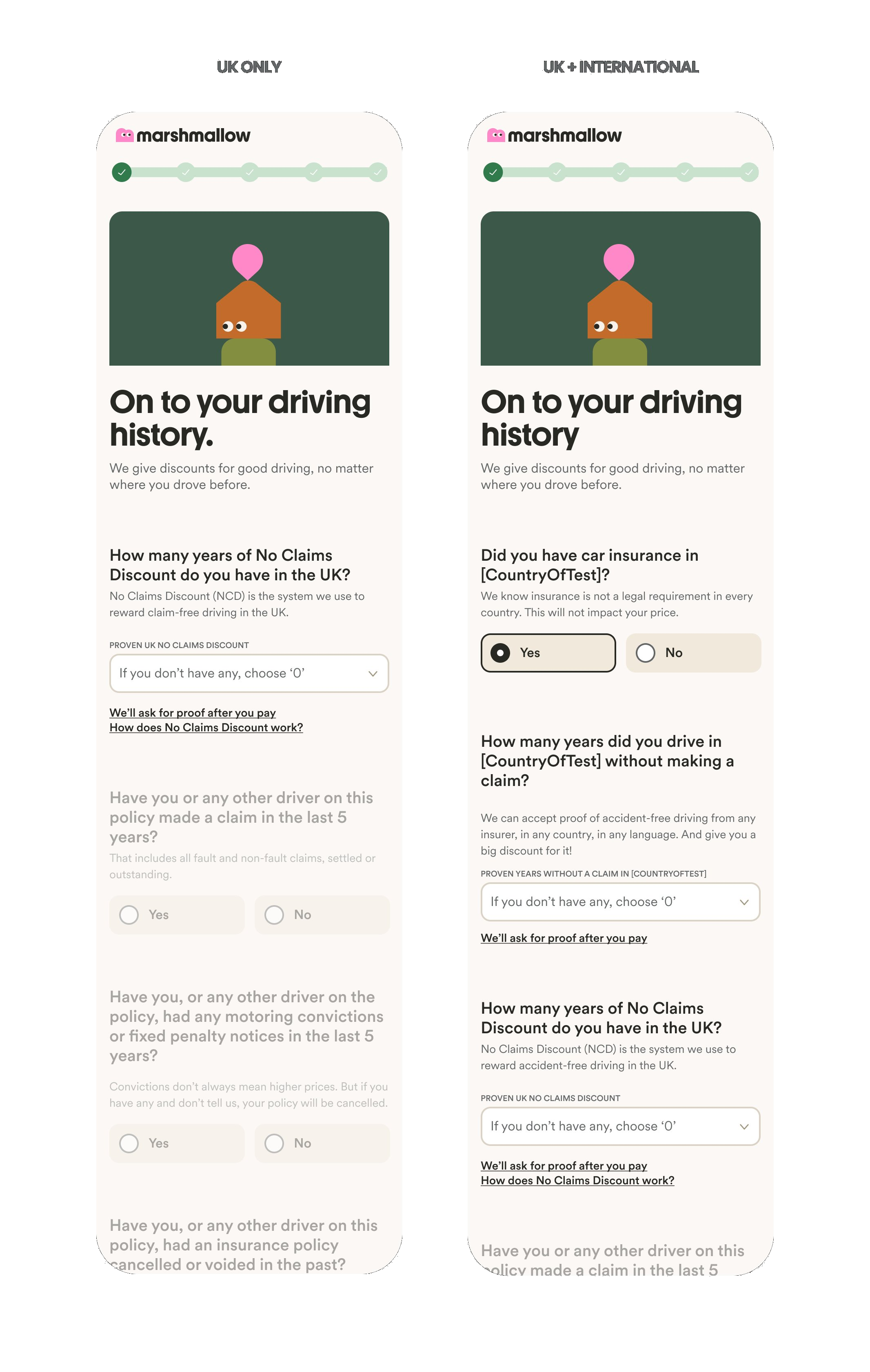

Recognition of "no-claims discount" was poor.

The concept exists in many countries, but under different names, processes and levels of regulation. Even customers with prior experience didn't always recognise the term, what they were declaring, or how the discount would work.

There's no one-size-fits-all label.

Phrases like "international NCD" felt clear to us but rarely to customers. Without already understanding what no-claims discount meant, those qualifiers tended to add confusion rather than reduce it.

People don't go looking for information they don't know they need.

To declare experience accurately, customers needed to understand eligibility and the validation process. We were making that information difficult to find, and the issues we saw downstream mirrored the content we'd deprioritised in the flow.

Customers are time-poor — guide them to the right outcome.

At sign-up, the priority isn't education. It's helping customers reach an accurate quote without having to learn the ins and outs of UK insurance. Better-targeted questions could do most of the eligibility checking for them.

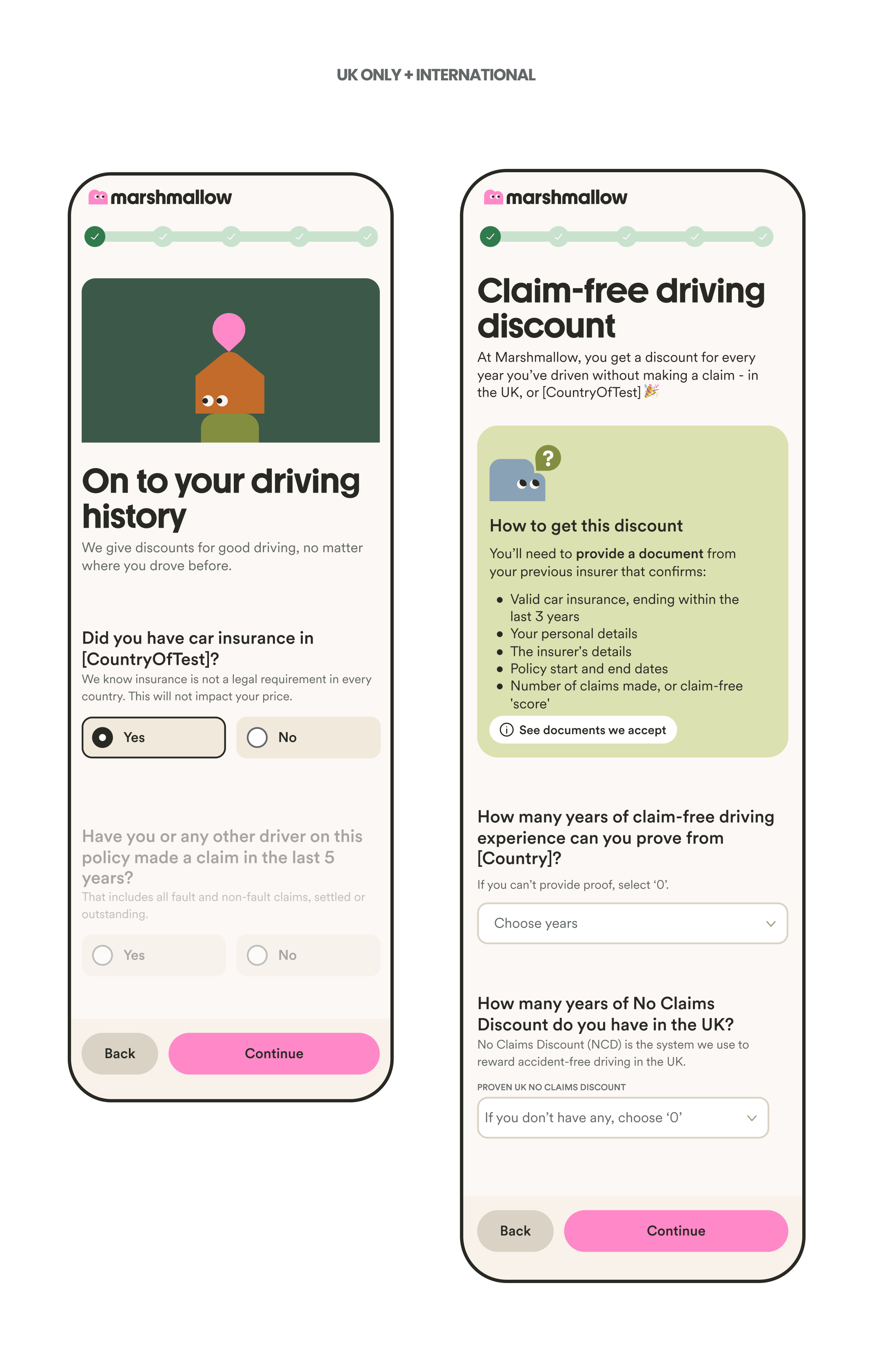

A new dedicated step, with eligibility upfront.

The first experiment was content-led: redesign the flow so that eligibility requirements were impossible to miss, and reframe the language around something customers could actually understand.

We introduced a separate screen for the no-claims discount questions, giving us space to set context and explain what we were asking before the customer had to answer. We moved away from old terminology and reframed it as a "claim-free driving discount" — plain, descriptive, and far more recognisable to our target audience.

We brought eligibility requirements to the top of the screen, added validation that flagged when someone's declaration was at odds with their licence information, and made it explicit that the discount is conditional on us being able to verify it.

Promising signal in the first cohort.

The first cohort to see the redesigned flow showed a roughly 20% reduction in first-month cancellations. Alongside that, fewer customers were declaring claim-free experience from other countries, the average years declared dropped, and the document upload rate went up.

We're treating this as a strong starting signal rather than a finished win. The experiment is one part of a longer programme of work, and there's more to test — how we communicate the benefit at acquisition, how we surface it at renewal, and how we filter sign-up content to better fit who's in front of us.